Twelve and a half million tourists visited Chiang Mai in 2023. The city’s accommodation sector ran at occupancy rates that, by the standards of the past decade, represent a solid recovery. Operators across hospitality, wellness, food, and experience filled their calendars, their rooms, and their tables. By every metric the Thai tourism system has historically been designed to reward, Chiang Mai had a good year.

The problem is that the metrics the system rewards are not the metrics Chiang Mai operators need to build durable, profitable businesses.

Over the past several months, CMBN’s research team has been working through the structural data behind Thailand’s post-pandemic tourism recovery, with particular focus on what the numbers reveal about the commercial landscape facing operators in Chiang Mai.

That work produced three editorial pieces published on this site, and a whitepaper, Thailand’s Wrong Competition, which examines the ASEAN competitive context in detail. What follows draws on all four to lay out the specific commercial implications for businesses operating in this city.

The system is working. That is the problem.

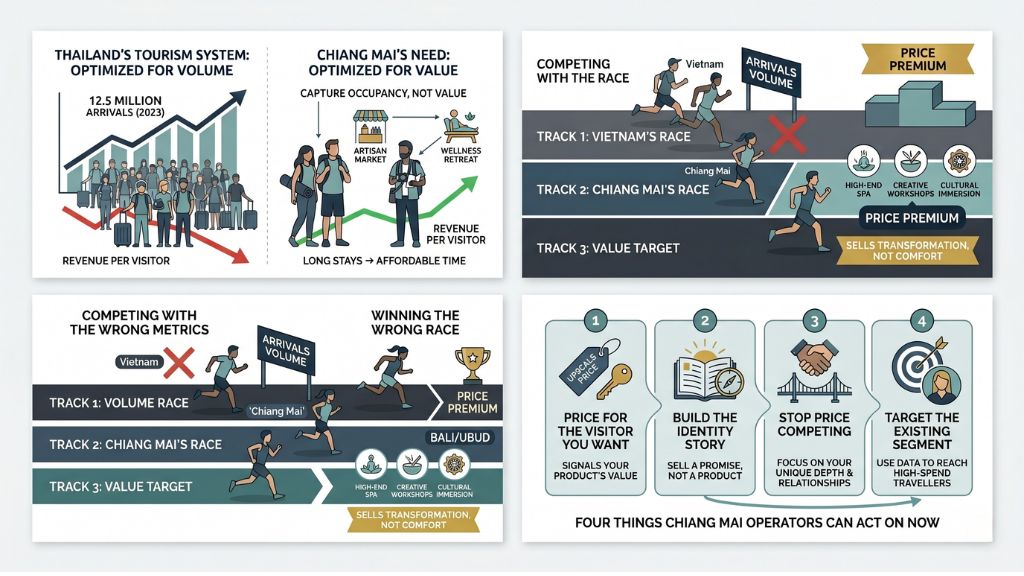

In Thailand Built the World’s Most Efficient Machine for Undercharging Tourists, the central argument is structural rather than operational. Thailand’s tourism architecture has spent decades optimising for a single metric: arrival volume. Infrastructure investment, visa policy, destination marketing budgets, airline route development — all of it flows toward the thing being measured. The result is a country that has become genuinely world-class at one task, getting people in, while the question of extracting value from those arrivals remains largely unaddressed.

This is not a failure of execution. The system is producing exactly the outcomes it was designed to produce. Between 2010 and 2019, Thailand’s international arrivals grew at nearly three times the global average while revenue per visitor barely moved. More tourists, each worth less. That pattern did not emerge by accident. It is what volume-optimised systems produce.

For Chiang Mai operators, this structural tendency shows up in a specific way. The visitors who spend the most per day — long-haul Europeans, wellness-focused travellers, cultural tourists with longer stays and higher daily budgets — are already here. They are not a missing segment. They are a present segment around which most of the city’s commercial infrastructure is not primarily organised or priced.

Chiang Mai is not competing with Phuket. It is competing with Ubud.

Winning the Wrong Race makes the case that Thailand’s tourism discourse is preoccupied with the wrong competition. The Vietnam comparison, which dominates regional tourism conferences and ministry briefings, is a comparison about volume and scale. It is a legitimate conversation for national tourism planners, but it has limited relevance for a Chiang Mai spa operator, guesthouse owner, or independent restaurant.

The competition that matters for Chiang Mai businesses is not Bangkok’s volume recovery or Vietnam’s arrival growth. The relevant comparison is with Ubud — not Indonesia as a whole, but the specific Balinese district that has, over fifteen years, built a global positioning as a destination where visitors do not simply rest but change. That positioning commands a price premium that has nothing to do with the quality of the physical product.

Bali Does Not Have Better Spas, It Has a Better Story documents this gap in detail. A four-night wellness retreat in Chiang Mai priced at 18,000 baht sits alongside a comparable Balinese retreat at three times that figure. The inputs are similar. The difference is in what each product promises the visitor about themselves. Bali sells transformation. Most of Chiang Mai’s wellness market sells comfort. These are not equivalent promises in terms of the prices they support.

Chiang Mai has every ingredient required to compete at the Ubud level. A meditation and mindfulness tradition with genuine historical depth. A food culture with distinct identity. A creative, independent business community that has been attracting exactly the kind of long-stay, experience-seeking visitor who generates high daily revenue. The gap is not in supply. It is in how that supply is packaged and priced.

What the data says about Chiang Mai’s actual position

Several specific data points from the research are worth sitting with as an operator.

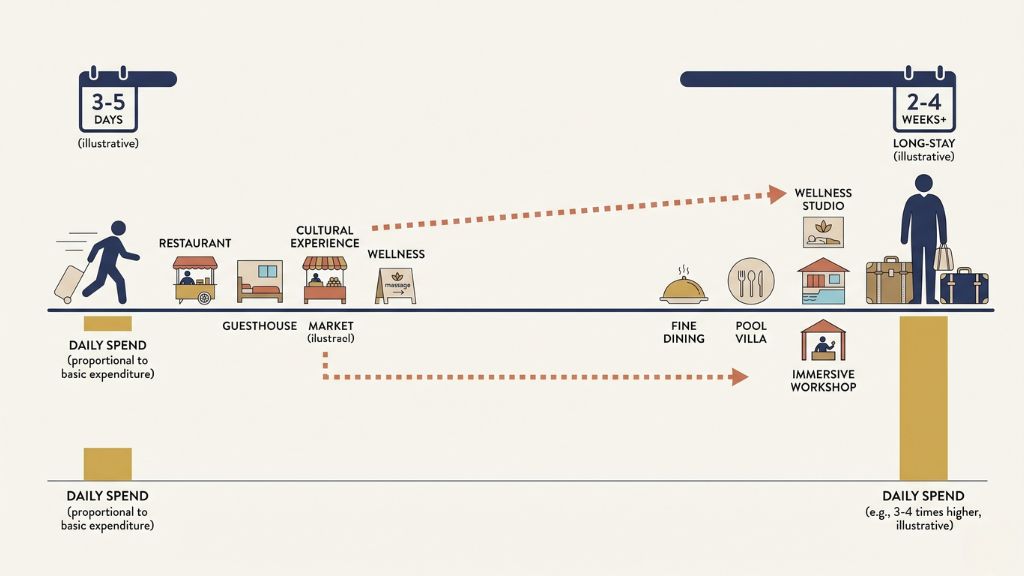

The average international tourist stays more than nine days in Thailand, which is among the longest average stays in the region. European visitors average close to 17 days. Long stays should produce high total revenue per visitor. In practice they do not, because the additional days are priced as affordable time. Operators are capturing occupancy without capturing value.

The segments generating the highest revenue per day are not the segments driving headline arrival numbers. Malaysian and Chinese short-stay visitors, while significant in volume terms, generate lower daily spend than long-haul European and premium wellness visitors. Chiang Mai’s commercial infrastructure is largely priced and marketed toward the former while the latter are present but underserved.

Chiang Mai was named the safest city in ASEAN in 2026 by Numbeo. The city’s smoke season aside, the structural case for Chiang Mai as a long-stay, wellness-oriented, premium experience destination is strong and getting stronger. The businesses that are already pricing and positioning to capture that visitor are not waiting for national tourism policy to change. They are making product and pricing decisions today that the data supports.

Four things Chiang Mai operators can act on now

The whitepaper’s argument closes on a point about system design: the shift from volume to value does not begin with a government campaign, it begins with what individual operators choose to measure and reward within their own businesses. The four moves below do not require waiting for anyone else.

Price for the visitor you want, not the visitor you have. If your current pricing is set to compete in a volume market, it is attracting a volume visitor. The long-stay, high-spend visitor who already exists in Chiang Mai is making booking decisions based on what your pricing signals about your product. Underpricing a premium experience does not attract more of that visitor. It repels them.

Build the identity story, not just the product description. The Bali premium is not built on better facilities. It is built on a promise about what the experience does to the person who has it. Chiang Mai operators with genuine depth in their product — cultural immersion, meditation instruction with real lineage, food experiences rooted in Northern Thai tradition — have the raw material for that story. Most are not telling it. Listing ingredients is not the same as making a promise.

Stop competing on price with operators who cannot match your depth. A guesthouse with genuine relationships in the community, access to local experiences unavailable to large hotels, and the ability to personalise a stay is not competing with a 200-room chain. Pricing as though it is competing with a 200-room chain destroys the margin that makes the personalised model sustainable.

Target the segment the data says is already here. European long-haul visitors, wellness tourists, and long-stay travellers are in Chiang Mai now. They are not an aspirational future segment. Marketing spend directed at attracting more of them, through channels and platforms where that visitor actually looks, is more productive than competing for the short-stay regional market on price.

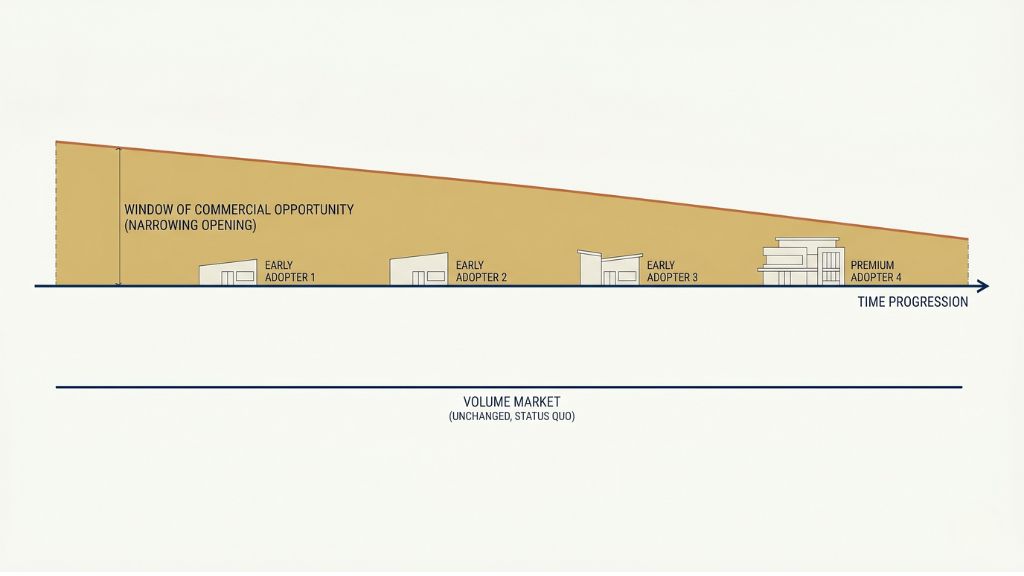

The city’s commercial window is specific

Chiang Mai’s strongest commercial position is not permanent. Ubud’s premium was built over fifteen years of consistent positioning, and it is now compounding in ways that are genuinely hard to displace. A city that starts building a coherent identity story now, priced and distributed to reach the visitor willing to pay for it, is building an asset. A city that continues to price for volume while its competitors price for value is not standing still. It is falling behind a market that is moving.

The data does not suggest Chiang Mai is in trouble. It suggests the gap between what Chiang Mai has and what Chiang Mai charges for it is a commercial opportunity that a specific group of operators is positioned to close. The businesses reading this are, by definition, the ones paying attention.

Read the full series: Winning the Wrong Race / Thailand Built the World’s Most Efficient Machine for Undercharging Tourists / Bali Does Not Have Better Spas, It Has a Better Story