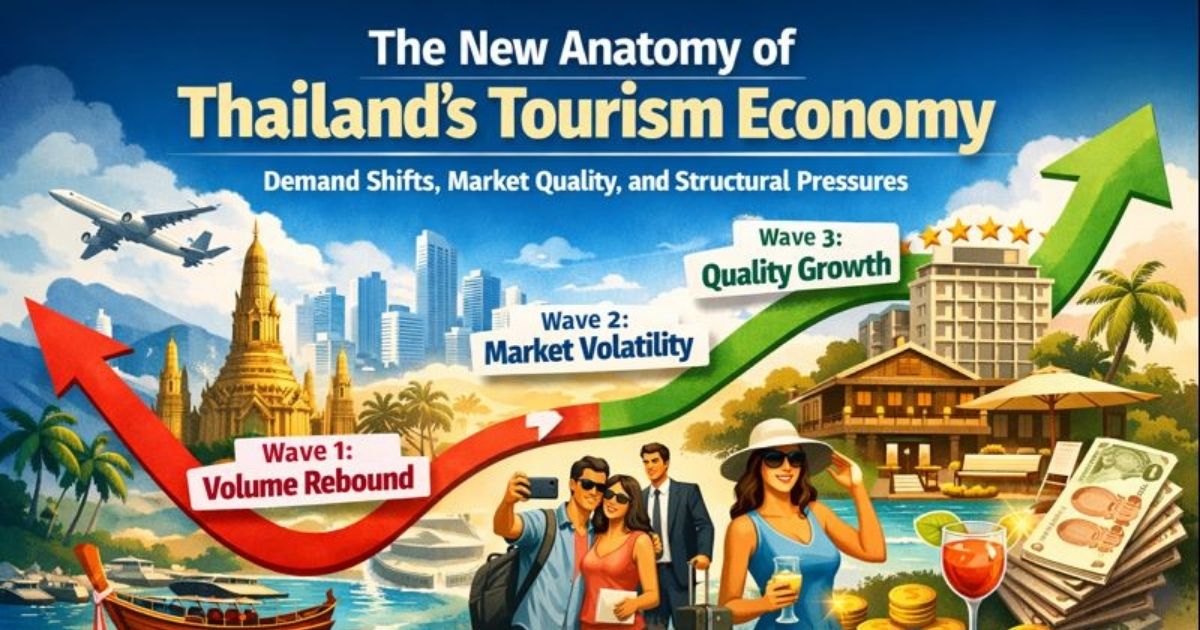

Demand Shifts, Market Quality, and Structural Pressures

Thailand’s post-COVID tourism recovery has not followed a straight line, nor has it returned to its previous form. Instead, the recovery has unfolded in three distinct waves, each shaped by global travel sentiment, macroeconomic forces, and structural shifts in Thailand’s competitiveness.

The result is not merely a rebound in visitor numbers, but a qualitative transformation that is setting a new trajectory for the industry over the next 2–3 years.

Wave One: A Volume-Driven Rebound After Reopening

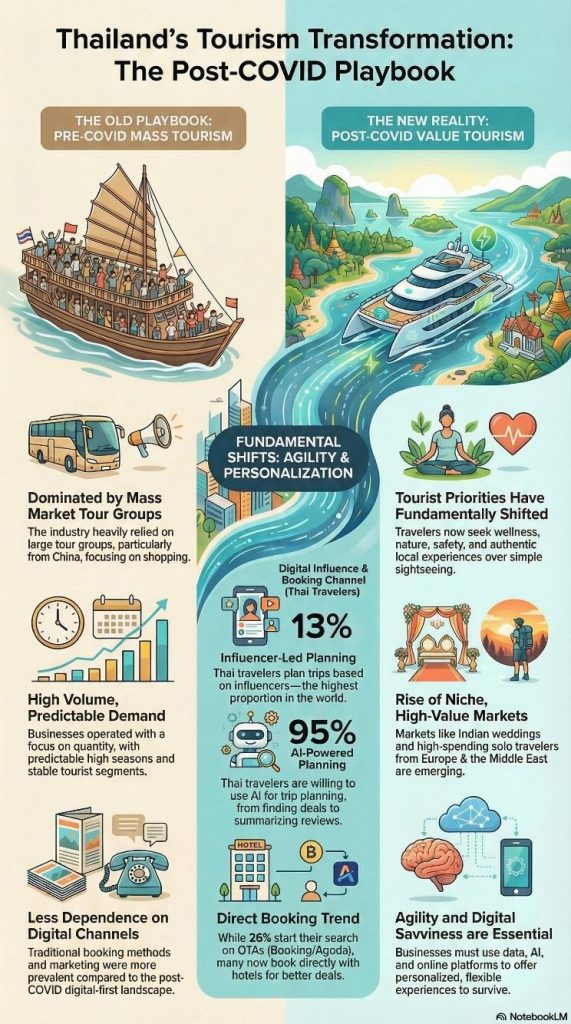

In the initial phase after borders reopened, Thailand saw a rapid surge in tourism demand driven by pent-up desire to travel after prolonged lockdowns. Visitor numbers climbed quickly, but revenues did not recover at the same pace, mainly due to:

• A disproportionately high share of short-haul travellers, particularly from East Asia

• Long-haul markets (Europe, the U.S.) remaining constrained by inflation, weak currencies, and high airfares

• Shorter length of stay and reduced spending per trip

• The aviation sector operating below full capacity, pushing airfares above pre-COVID levels

This phase was, in effect, a “fast but fragile” recovery—visitor volume returned, but spending quality and total receipts remained significantly below 2019 benchmarks.

Wave Two: Fragmented Markets, New Behaviours, and Heightened Volatility

By 2023–2024, travel demand evolved into something more diverse and complex. Several trends became evident:

• Thai travellers continued to travel actively, despite weakened purchasing power

• International tourists increasingly shifted toward higher-spending markets such as the Middle East, Europe, and Australia

• AI became a mainstream tool for planning, comparing, and booking trips

• OTAs remained the primary research channel, but Thai travellers increasingly booked direct with hotels to secure better value

• Demand for high-quality experiences grew, even as price sensitivity remained high

On the supply side, hotels reported a steady improvement in occupancy:

• Oct 2025 → 63% average occupancy

• Nov 2025 (forecast) → 67%

Yet several risks remained prominent:

• Labour shortages, particularly in Northern and Northeastern regions

• Rising costs—food, energy, and wages

• Safety concerns affecting inbound demand

• China’s recovery remained incomplete across flights, spending power, and travel patterns

This phase represents a market in rebalancing, still vulnerable to macroeconomic shocks and rising operating costs.

Wave Three: Quality-Driven Growth and Strategic Competition

The year 2024 marked the beginning of a genuine qualitative upturn. Key indicators signal strong momentum:

• 35 million international arrivals — exceeding expectations

• Tourism revenue surpassing 1.8 trillion THB

• Strong performance in premium and luxury segments (France, Middle East, Israel)

• Some visitor groups spending up to 100,000 THB per trip

• Millennials (Gen M) spending nearly 9,941 THB per trip, prioritising value-rich and experiential travel

A major catalyst has been the strategic expansion of international air routes, including:

• Paris – Phuket

• Abu Dhabi – Bangkok

• Tel Aviv – Phuket

Long-haul travellers brought in by these routes tend to stay longer, spend more, and exhibit stronger destination loyalty, thus enhancing Thailand’s overall tourism yields.

Simultaneously, personalised hospitality has emerged as a new standard. More than 80% of Thai travellers expect customised experiences, while foreign visitors increasingly use AI to curate their stays. Competition is therefore shifting away from price battles toward data-driven, personalised service delivery.

Macroeconomic Summary: Clear Opportunities, Persistent Risks

Despite the positive trajectory toward higher-quality growth, several structural risks remain:

• Rising operating costs

• Heightened safety and image concerns

• Slower global economic momentum

• China’s recovery still below pre-COVID levels

• Weakened domestic purchasing power due to high living costs

This means Thailand must compete not by volume alone, but through experience quality, safety, and value for money—the new pillars of competitiveness in global tourism.

From Chiang Mai to Thailand: Local Signals That Reflect National Structural Shifts

Insights from the Travel Link 2025 seminar—initially framed through the lens of Chiang Mai —serve as a microcosm of Thailand’s broader tourism challenges and opportunities. What emerged at the city level is now visible nationwide:

• Recovery remains incomplete: demand is back, but its structure has changed

• China no longer behaves as the pre-COVID “default engine” of inbound tourism

• Destinations succeed when they attract quality segments—long-stay, digital nomads, premium travellers

• High airfares and limited direct flights remain structural bottlenecks

• Destination awareness matters more than expected; even strong destinations can fall “off-radar”

• Businesses increasingly rely on real data, not just historical assumptions

When zooming out from a city to a national lens, Chiang Mai becomes a test case for the structural forces shaping Thailand as a whole—market shifts, competitive pressures, access constraints, and the growing need for data-driven strategy.

In other words: What happens in Chiang Mai is not a local anomaly—it is a structural signal for the future of Thailand’s tourism economy.

References & Data Sources

1. Bank of Thailand

2. Tourism Authority of Thailand

3. Bangkok Biz News

4. Thai Hotels Association

")